One question that’s come up several times over the last couple months centers on whether your portfolio should change after you retire. In fact, one person I’ve spoken with recently assumed that once he retired, his advisor would by default sell all the stock funds in his accounts and replace them with income producing bonds.

Typically the longer your time horizon, the more risk you have the capacity to take in your investment portfolio. Most people in their 20s and 30s have a high capacity to take risk, since they have a long time until they’ll need to live off their savings. A significant portfolio loss won’t impact their life, and they have a long time to recover. Because of that, many choose to hold mostly equities in their retirement accounts since they’ll provide the greatest long term returns.

The closer you get to retirement, the lower your capacity to take risk. Prudent investors tend to shift their asset allocations more and more toward bonds as this progression evolves. But for most people it should level out at some point. Most of us will need some growth out of our portfolios in retirement if our assets are going to last the rest of our lives, meaning that we probably don’t want to be 100% in bonds.

But how should our investment strategy change when transitioning from the accumulation to the distribution phases of our lives, and should it change at all? This post will explore the issues, and what you might consider when making the transition yourself.

Income vs. Total Return Investing

Before we dive in, an important concept to understand is the difference between income and total return investing. If we were going to invest for income, we’d try to build a diversified portfolio of income producing assets like bonds, dividend paying stocks, or real estate investment trusts (REITs). Ideally we’d be able to generate enough income from the portfolio to meet withdrawal needs, meaning that you’d never need to sell securities to generate any additional cash.

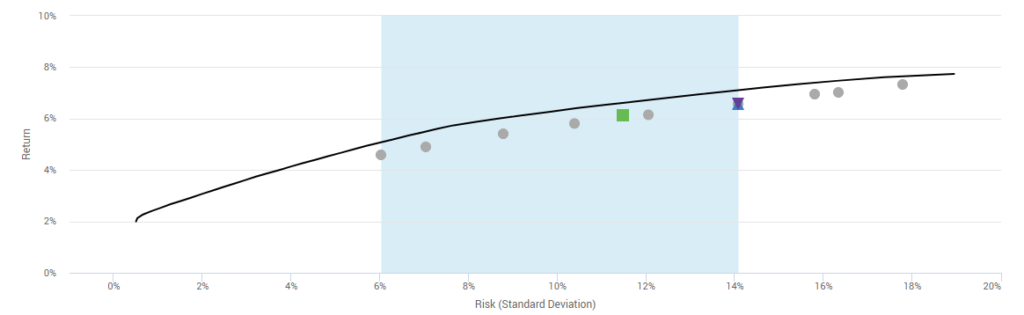

Total return investing is a little different. Rather than focus on income producing assets only, a total return approach focuses on producing the best risk adjusted return possible. There’s always a trade off between risk and return. It’s perfectly fine if you don’t have the capacity or interest in taking much investment risk – we can build a portfolio for that. It’s also perfectly fine if you want to shoot for the moon & grow your assets as much as possible. We can build a portfolio for that too, but you’d need to understand that it’ll come with quite a bit of volatility. Regardless of where you fall on that spectrum, the idea is to maximize the return you receive for any level of risk. (Or alternately, minimize the amount of risk you’re taking for any unit of return). We can express this graphically, and it’s called the “efficient frontier”. The line in the chart below represents the efficient frontier, and the greatest amount of expected return for each level of risk. It’s not possible to build a portfolio that falls above the line.

The Efficient Frontier

For a portfolio to fall exactly on the line above (and maximize the expected return per unit of risk), it must be free from investment constraints. For example, the FANG stocks – Facebook, Amazon, Netflix, and Google, have produced a great portion of the US stock market’s returns over the past several years. All four are rapidly growing companies, and reinvesting the lion’s share of their profits back into their companies to fund expansion initiatives.

None of these four stocks pay a dividend. Investors building income portfolios of bonds and dividend paying equities would have omitted the FANG stocks entirely, missing out on some wonderful returns.

A total return approach doesn’t discriminate against growth & non dividend paying companies. Rather than rely on the income that’s distributed back to shareholders and bondholders, total return investors simply sell holdings in the portfolio monthly/quarterly/annually as needed to raise the cash desired by the investor. Total return investors don’t miss out on the investment opportunities that income investors do, and should therefore enjoy better risk adjusted returns.

Now, comparing income investing to total return investing is not completely apples to apples. Income investors tend to rely stocks that pay qualified dividends, and bonds that make consistent interest payments. While bond interest is taxed the same as ordinary income, qualified dividends are taxed at lower rates. For total return investors, the primary source of taxation is capital gains on investments sold. Positions held for longer than 365 days qualify for favorable long term rates, while short term capital gains (anything held less than 365 days) is taxed as ordinary income.

Other Tax Considerations

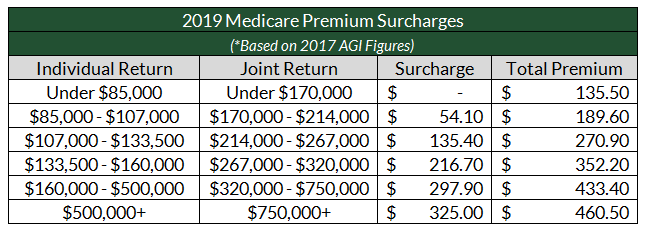

Keep in mind here that portfolio income won’t just impact your marginal tax bracket. While it won’t matter in an IRA/401k/Roth accounts, income produced in taxable accounts could cause you to pay Medicare premium surcharges, and potentially the rate you pay on long term capital gains. Remember that Medicare premium surcharges are based on your adjusted gross income from two tax reporting cycles prior. Here’s the chart for 2019:

And here are the long term capital gains brackets for 2019:

Chances are low that the decision of whether to structure your taxable accounts for income or for total return will affect your medicare premium surcharge or long term capital gains rates. But it could given the right circumstances. The moral of the story here is that it’s important to understand how changes to your portfolio might impact the other areas of your finances. The best way to do this, of course, is to build a comprehensive financial plan & multi-year tax projection.

The Verdict

Transitioning from the accumulation to the distribution phase of life usually comes with a change in investment objectives. While you’re probably seeking portfolio growth in the accumulation phase, the distribution phase typically comes with a need for income. But that doesn’t mean your portfolio needs to change. Approaching your investment strategy with a total return mindset – both before and after retirement – will lead you to better returns over the long run. Yes, you should probably take less investment risk the closer you get to retirement. But the best allocation and best portfolio for you will depend on your personal objectives and need for growth. All of which should be spelled out in a comprehensive financial and retirement income plan.

What do you think?

Did you or your advisor alter your portfolio once you stopped working? Why or why not?