Let me start by saying that I’m a big fan of most tax preparation software. Taxes are a cost in and of themselves. Any way to automate the prep and filing process in a compliant and inexpensive way is A-OK in my book.

But even though they’re easy to use, Turbotax and others are still software programs that have limitations just like any other robot. When your financial picture becomes sufficiently complicated, spending the extra cash to hire a professional can actually save you money in the long run. Here’s my take on when you should ditch the software for an experienced professional.

What You Should Know About Tax Prep Software

When people talk about tax in general, there are really two sides to the conversation: tax planning and tax compliance.

Tax planning is essentially planning transactions before they happen, and making thoughtful decisions that will minimize the total amount of tax you owe. Tax compliance, on the other hand, has to do with preparing your return, filling out forms, and reporting on transactions that have already occurred.

While tax prep software is great and all, it’s really only useful for tax compliance. The more complicated your financial profile becomes, the more decisions you’ll have to make, and the more important tax planning will become.

Here’s an Example:

Jason is a 25 year old college graduate who’s just started his first job at a big architecture firm. He makes $60,000 per year in W-2 income, rents an apartment with a roommate, and contributes to his 401k.

Jason’s financial profile is pretty straight forward. He could reduce his tax burden by contributing more to his employer’s 401k, an IRA, or potentially a health savings account (if he was enrolled in a high deductible health plan). But outside of those options there’s not much planning to be done, since there are simply not many ways he could report his income. Yes he could claim some deductions here and there, but that’s nothing that tax prep software can’t handle.

Now let’s fast forward 25 years. Jason’s situation has changed quite a bit. He quit his job to start his own architecture firm, which has done quite well. He bought a house with his wife, and they also own several rental properties.

Jason would probably want to consult with a CPA. He has flexibility in how he runs his business, meaning there are many decisions to be made and potential planning opportunities. And since he has income from the rental properties (which he’s depreciating to offset income) along with other large deductions like the interest on his mortgage and his home office, it’s likely that the value a CPA would bring would exceed their out of pocket cost.

Here’s Why I Like Tax Prep Software

Filing your taxes is really a tax compliance function. You’re reporting on transactions that have already occurred – namely the income you received over the prior year less any deductions. The end result is your income for the year, which of course is what the amount of tax you owe is based on.

The preparation and filing of your return is a very operational job. You compile data, fill in the boxes, sign your return, and mail it off. Go figure, this is something computers are really good at. There is potential for human error if you file taxes the old fashioned way, and for a small cost tax prep software eliminates most of that risk.

Most software has the functionality to import and compile your tax documents (like W-2s and 1099s) too, so you don’t even need to key in the data. Earlier in my career, there were years when I filed a return through TurboTax in less than 20 minutes. And even better, in the years I received a refund, the funds were deposited in my account no more than a few days later.

Audit Protection

One of Turbotax’s unique features is a premium service called “Audit Defense.” Basically, for an extra $40 Turbotax will handle all correspondence with the IRS if you get audited. A licensed tax professional would represent you by:

- Developing a plan of action

- Following up with the IRS

- Preparing IRS documents for you

- Representing you in all IRS meetings

This is a pretty nice feature for $40, and ensures some professional guidance if you do get audited. But – keep in mind that audit defense doesn’t protect you from improper inputs on your return, like claiming fraudulent deductible expenses or omitting 1099 income. While TurboTax will be responsible for the correct preparation and filing of your return, you’re still on the hook for everything that goes into the calculation.

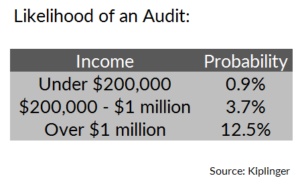

For context, the chances you’ll actually be audited are pretty slim. Many people even go their entire lives without being audited by the IRS. When selecting who to audit, the IRS looks for odd-looking returns and income level relative to your personal profile.

From our example above, Jason has a very ordinary return at age 25, meaning his chances of being audited are pretty low. 25 years later his return is certainly more complicated, but not out of the norm for a 50 year old who files jointly with their spouse. If he’d filed his 50 year old return at age 25, his chances would be far higher.

Other Tax Prep Software

Although I keep mentioning Turbotax, there are plenty of tax prep choices on the market today. Turbotax is just the market leader. By most accounts (reviews.com & Kiplinger, for example) it’s about the best of what’s available. TaxAct, H&R Block, and Tax Slayer all have competing products, which I’m sure get the job done just fine.

What You Should Know About CPAs

First off, keep in mind that a CPA isn’t the only type of professional who can help you with your taxes. Certified Public Accountants are accounting professionals who have passed a series of exams, have minimum experience in tax and audit, maintain continuing education requirements, and in most states also have a bachelor’s degree. (In fact, in some states you’re not allowed to call yourself an “accountant” unless you’re a licensed CPA).

Enrolled Agents (EAs) are also legally recognized tax practitioners. EAs are also required to pass an exam and undergo continuing education. But whereas CPAs are regulated on a state to state basis, EAs are regulated by the federal government, as the credential is awarded by the IRS.

To sum up the difference between the two, EAs usually focus on tax preparation and resolution. They’re authorized by the Department of the Treasury to represent taxpayers before the IRS for audits and other issues, but may not be well versed in tax and accounting issues businesses are faced with. The education and experience required to become an EA is also quite a bit lower than it is to become a CPA, as anyone who passes the exam can be awarded the designation.

CPAs on the other hand are usually more business focused. Many have experience in bookkeeping and expertise in tax matters beyond your personal return. If you’re a small business owner or need some long term tax planning help, you’ll probably want to speak with a CPA. But if you’re considering a professional for the very first time and only need someone versed in tax reporting and compliance, you may be able to save a few bucks by hiring an enrolled agent who’s not a CPA.

The Benefit of Hiring a Professional

Whereas software is an inexpensive and efficient way to tackle tax compliance, it’s severely limited when it comes to tax planning. And for most people, tax planning becomes more important as their financial picture grows more complex. All of a sudden they’re faced with more and larger financial decisions, the ramifications of which will have a big impact on how much tax they pay over time.

Yes, tax prep software can give you an answer into how a certain decision might impact your taxes (will choice A or choice B result in more tax?), but it’s very black and white.

As the number and magnitude of decisions you have to make grows, professional expertise can become very helpful to see the picture clearly. Over time, thoughtful planning becomes necessary if you want to minimize the amount you fork over to Uncle Sam, and its simply a job that computers can’t handle. At least until artificial intelligence takes over tax work.

When You Should Hire a Professional

So what are some examples of tax planning opportunities? What “red flags” should you look for?

It varies for everyone, and if you’re well versed enough in the tax code to identify these opportunities and make adequate planning decisions, you probably don’t need to hire a professional at all. But, most people I know prefer to spend their free time on activities that don’t involve mastering the tax code.

Here are common life events that often yield planning opportunities:

- You have or are starting a small business

- You have or are buying rental property

- You’d like to begin planning for future generations (estate planning)

- You have material foreign income

- You are or in the past have been subject to the alternative minimum tax (AMT)

- When you’re making a big life change like retiring or buying into a partnership

- You’re unsure whether to accelerate or postpone income

- You have restricted stock or employee stock options

- You’re not sure how much to withhold from your paycheck or pay in quarterly estimates

Again, anyone can file their own taxes with or without the support of Turbotax or other software. But when tax planning opportunities arise, some careful forethought can go a long way.

If you do go the route of hiring a professional, make sure that they’re communicative with your other professional advisors (financial planner, investment manager, estate planning attorney, insurance professional, etc.). Taxes are a big part of the picture, and should be integrated with your financial plan. It’s essential that whomever you hire shares the same vision of what that plan is with you and your other advisors.

What do you think? What’s your preferred tax prep software? What might cause you to hire professional for help with your taxes?